Paycheck advance apps: The benefits and dangers

Do you need cash fast? No need to head to a bank or payday lender.

Paycheck advance smartphone apps are growing in popularity as a way to quickly get money when you’re in a jam.

While these apps can be helpful in some situations, Consumer Reports warns there are potential downsides you need to know about.

Paycheck advance apps allow you to request some portion of your next paycheck before payday, and there’s usually a fee or subscription cost ranging from $1 to $10.

Then on payday, the advance is recouped by debiting the money from your bank account or directly from your paycheck.

These services can be great to help you out of a jam here or there.

But you have to be careful not to make it a habit.

If you end up using these services regularly, the fees you pay can add up.

Research has shown that people who use these apps tend to take out advances regularly.

And because the apps are heavily used by minimum wage workers, that means they sometimes end up in a vicious cycle of borrowing.

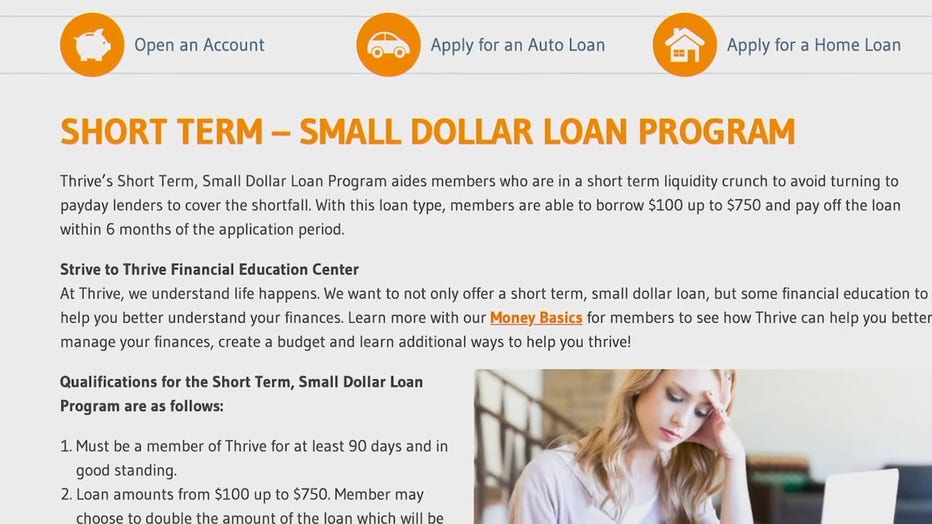

So if you find yourself coming up short in paying the bills every month, consider looking for a bank or credit union that offers short-term small-dollar lending services.

The APR on these loans generally don’t exceed 36 percent, and they can also help you build your credit.

Cash advance situations can always have high credit problems, and you want to be very fiscally responsible when you’re looking at any of these types of things.

MoneyLion tells Consumer Reports that its app helps its members pay bills and avoid overdraft fees, and gives them greater control over their finances.

All Consumer Reports material Copyright 2021 Consumer Reports, Inc. ALL RIGHTS RESERVED. Consumer Reports is a not-for-profit organization which accepts no advertising. It has no commercial relationship with any advertiser or sponsor on this site. Fo