New advice on rental car insurance

Planning a trip that includes a rental car? Finding the right size car is easy, but what about insurance add-ons? Should you buy the added coverage? Or are you already covered with your

own policy? And If you think your credit card will always cover you, think again. Consumer Reports reveals money-saving tips on rental car insurance.

Consumer Reports says before you rent a car check for coverage under your personal auto insurance. And also, through the credit card you’ll use. Credit cards can change their terms. For instance, Discover recently stopped offering rental car insurance altogether. American Express, Chase and Citibank still do offer it but check their terms and limits. If a credit card is your primary coverage, there could be a benefit to using it.

Should there be a claim, the credit card insurance could be in line to cover it and your own auto insurance rates may not change.

Remember that to be covered through your credit card you need to pay for the entire rental with that card and decline the rental agency’s coverage.

However, if you are going to depend on your own auto insurance policy remember the rental will be covered under the same terms as your own car. So check those terms carefully. For

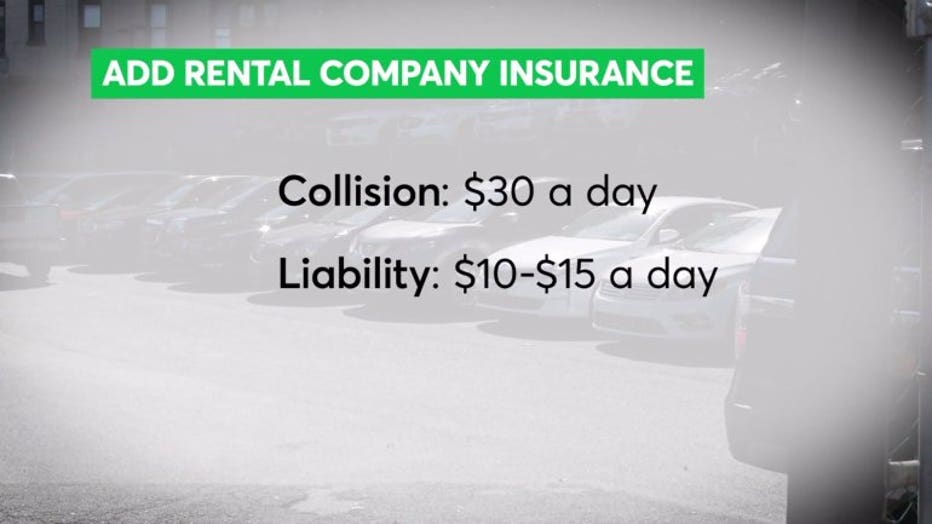

instance, if your personal policy doesn’t have collision coverage, you should consider adding the rental car company insurance. But that can run as much as $30 a day and liability can run $10 to $15 a day.

If you are traveling outside the U.S., it’s very possible your personal insurance won’t cover a rental car. In that case, your best option may be to get the rental company’s insurance. Read the terms carefully and make sure it will cover your anticipated itinerary and activities.

All Consumer Reports material Copyright 2018 Consumer Reports, Inc. ALL RIGHTS RESERVED. Consumer Reports is a not-for-profit organization which accepts no advertising. It has no commercial relationship with any advertiser or sponsor on this site. For more information visit consumerreports.org.