Americans’ personal savings rate nears all-time low, economic analysis shows

The rate at which Americans are saving money has dipped close to an all-time low, a new report shows.

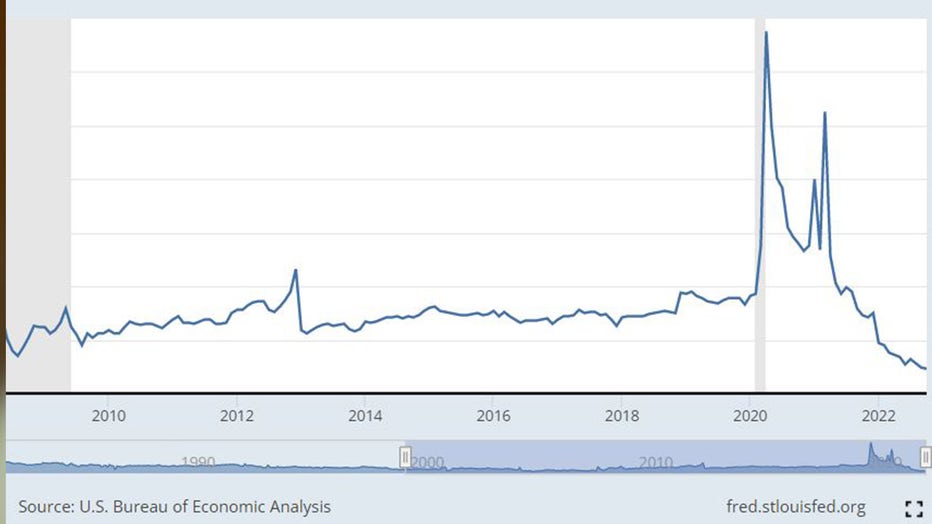

According to the U.S. Bureau of Economic Analysis, the personal savings rate dropped to 2.3% — down from 7.3% a year earlier and down from 33.8% in April 2020.

In fact, this is the lowest rate since July 2005 when the rate hit a record low of 2.1%.

The U.S. personal saving rate is personal saving as a percentage of disposable personal income. In other words, it's the percentage of people's incomes left after they pay taxes and spend money, the agency explains.

According to the U.S. Bureau of Economic Analysis, the personal saving rate dropped to 2.3%.

During the COVID-19 pandemic, the saving rate rose significantly. With restaurants and entertainment venues closed, experts say, Americans had fewer things to spend money on.

"The current low savings rate mostly reflects higher current consumption that was postponed due to the pandemic," Arabinda Basistha, an economics professor at West Virginia University told FOX Television Stations. "The extra savings and fiscal support during the pandemic are driving the higher consumption."

He continued, "The other indicators of financial health of American families look quite stable and able to withstand moderate risks to the economy. For example, the financial obligation ratio, measuring payments on debt service, rent, auto lease, homeowners' insurance and others as a percentage of disposable income, is 14.3 percent in the second quarter of 2022. This is lower than the average 14.8 percent in 2019, and the average 17.6 percent in 2005-2007 before the great recession."

Americans’ saving accounts starting to dwindle

A study released by Northwestern Mutual 2022 Planning & Progress earlier this year revealed a solid majority (60%) of Americans say they’ve been able to build up their personal savings over the last two years — but it’s dwindling.

Year-to-year numbers showed the average amount of personal savings dropped from $73,000 to $62,000 between 2021 and 2022.

But other studies paint an even more dire picture when it comes to Americans and their savings accounts.

In June, the Federal Reserve reported that 36% of Americans do not have enough money to cover a $400 emergency expense.

Financial experts have even weighed in on the financial state of many Americans.

"In 2022, Fidelity’s Financial Wellness Checkup surveyed adults we administer employer financial benefits for and found less than one in two had enough emergency funds to cover a typical three months living expenses," Megan Moore, vice president for Fidelity Bloom, told FOX Television Stations. "And nearly one in four had less than one month's worth of living expenses saved."

What are the challenges to Americans saving money?

Several factors can inhibit a person’s capability to put away money for a rainy day.

In 2016, The Atlantic proposed several theories on why Americans have trouble saving. Factors can include lower salaries, mortgage debt, and materialism.

Moore said some people may have trouble balancing the enjoyment and necessities of life.

RELATED: Here’s how much money you should be saving per paycheck

"First, people are having a hard time finding the right balance between how they live an enjoyable lifestyle today while also setting aside money for the future," she said. "Many people mistakenly believe you can only really have one or the other, but not both at the same time."

Moore added, "Second, managing week-to-week cash flow can be a challenge. When the money you earn, spend, and save is all intermingled in the same accounts, it can be really confusing to detangle how much you have available on a given day to safely spend and how much you shouldn’t touch and put towards saving."

How can Americans start to save?

Moore said for those who live paycheck-to-paycheck, putting away any amount of money counts.

"The easiest way to get started saving is setting it on autopilot," she said. "Create an account for money that isn’t meant to be spent unless it’s an emergency, and set up automatic transfers to deposit a portion of your paycheck or money from an existing bank account in regularly."

Other experts also share similar sentiments.

RELATED: Personal loan interest rates continue trending down for 5-year fixed-rate loans

"When you're starting a savings plan the best way to handle it is to decide that you're going to put a little bit of money aside or set up with your payroll where you're going to put $200 $250 or whether it be $500 — start small and have that money put into another account at a separate bank outside of where you normally spend and have your bills coming out of," Randy Jones, a wealth financial advisor based in Northern Virginia, told FOX 5 DC. "When you get to the end of the month, if you haven't touched that money, then you know that you can start saving that and consistently build on that to restore your savings if you had to dip into it."

This story was reported from Los Angeles. Chris Williams contributed.